Overview

This case study touches upon how can we create a digital banking experience for children as young as 6 years old; allowing them to start banking on their own.

This study takes into account the age range of the primary target users (children) with guided access from the secondary target users (parents), and the financial as well as cultural aspects of the demographic region.

My Role

Product Design, UX Research, UI Visualisation

Methods & Tools

Competitive Analysis, User Research, Interaction & Visual Design, Prototyping, Adobe XD

Date

Jan 2021

Research

In order to build a product and experience revolving around digital technology, money and children, it’s important to first understand about our target user behaviour. Spending and shopping online, transferring money using apps or computers may seem almost like second nature to us adults, but one may wonder how much exactly can a child comprehend and navigate around money and technology, especially in this day and age.

Financial Literacy

Many children receive a regular “income” in the form of ‘pocket money’ and thereby, many children’s understanding of income is shaped by this cultural practice. Hence, there is already some form of exposure to the concept and value of money.

In fact, one study from the University of Cambridge found that

money habits in children were formed by the age of 7

Source: “Habit Formation and Learning in Young Children” by Dr. David Whitebread and Dr. Sue Bingham University of Cambridge.

Children ages 8-12 exhibit new skills and thought patterns, and by the end of this developmental stage, they should achieve the milestone of logical thought, allowing them to understand the concept of cashless money transactions.

Tech Savviness

Today’s young children are brought up exposed completely to technology, giving rise to the term “digital natives”. Children aged 3-5 tend to spend around 4 hours per day with technology. Other age groups are showing an increase in the amount of time spent as well.

Statistics tell us that 45% of 8-11 year olds use social networking sites. Many parents admit to asking their children and teenagers for help with problems on their phones or tablets, and even younger children demonstrate remarkable skills with computers.

In research by Ofcom,

Source: “Tech-Savvy Toddlers: Why are Young Children So Good With Technology?”,

(February 2018) Southern Phone Co. Aus

Product Analysis

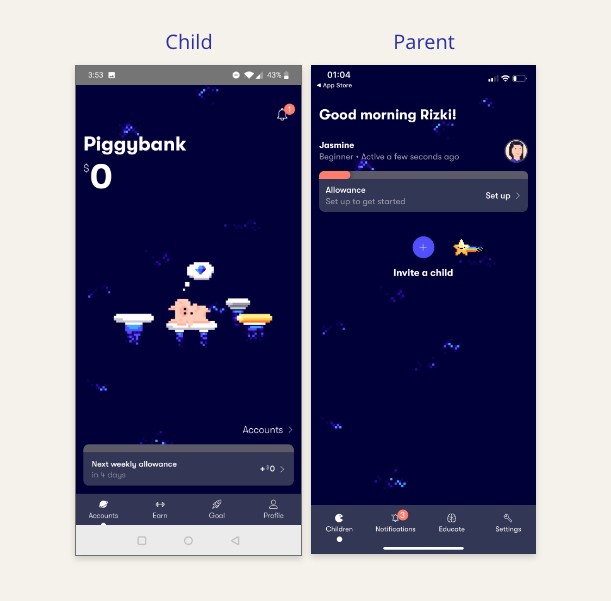

Gimi

Sweden

Gimi is an educational app that teaches children and young adults about money.

Pros

Prepaid Card is available (MasterCard)

Very interactive with appealing visual designs and animations

Gamification via quizzes and achievements on financial education

Chore Request/Tracker available

Basic interactive Chatbot

Cons

Limited currency options

UI can be a little complicated for younger children

Link to bank account unavailable

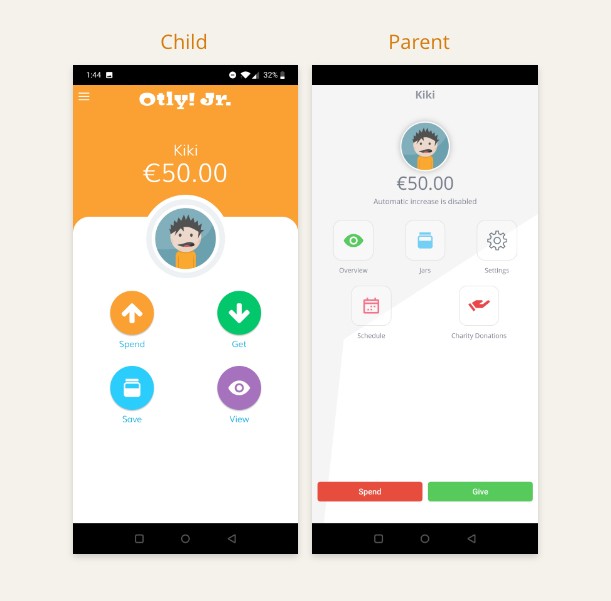

Otyl! Jr

Netherlands

Otly! is a free platform that modernizes the way families handle pocket money and teaches children the responsibilities that come with it.

Pros

Can link to bank account (only Parent access)

Can purchase giftcards (only Parent access)

Option to donate to charity

Simple and clean UI, easy to navigate especially for younger children

Cons

Very limited currency options

No Prepaid Card available

No Chore Request/Tracker

Child access and Parents access are in 2 separate app; Otly! Jr and Otly!

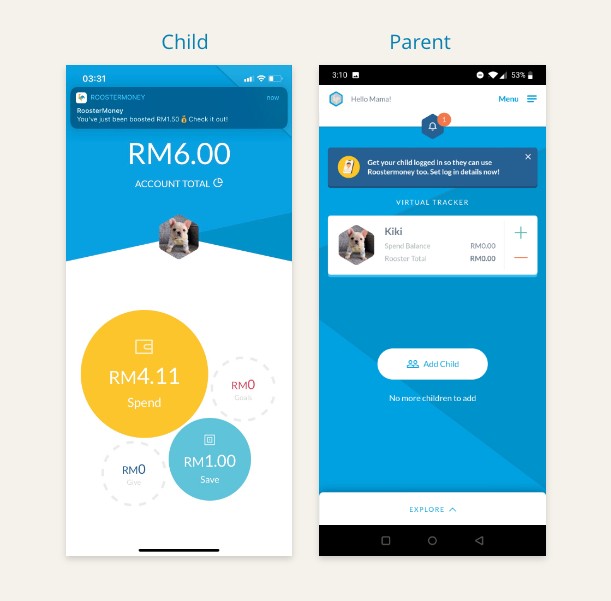

RoosterMoney

United Kingdom

RoosterMoney helps families keep track of pocket money and helps teach children to save responsibly.

Pros

Prepaid Card is available (Visa)

Chore Request/Tracker (with PLUS plan)

Nice and clean UI, easy to navigate

Option to donate to charity

Available in several different currency options including MYR

Cons

Link to bank account unavailable

Spend, Save and Give pots can be a little confusing and redundant

Additional charges to unlock Chore Request/Tracker feature

User Research

As this experience will be an introductory exposure to children on their first financial management learning, a lot of hand-holding from parents/guardian is to be expected. Also, as they are not adults yet, parent/guardian supervision and permission are legally required.

Hence, this experience is not limited to just children but also extends to those of parents and guardians as users.

User Persona

Arvind Daniel

10 years old

Student (Primary 4)

Loves games and sports especially football

Gadgets

Laptop

Budget smartphone

Favorite Apps

YouTube

PubG Mobile

TikTok

Pain Points

Loses track of how much allowance money he’s asked from his parents

Has to rely on his parents and constantly ask for money from them

Motivation

Save up enough money for new football shoes

Top up game credits

Hang out with friends and buy snacks and boba tea

Susan Tanuwijaya

42 years old

Career Woman and Mother

Enjoys coffee and reading

Gadgets

Laptop

Smartphone

Tablet

Favorite Apps

Grab

Lazada

Kindle

WhatsApp

Pain Points

Her children tend to overspend and always ask her for more allowance money

Busy and sometimes forgets/loses track of her children’s allowance

Motivation

Teach and instill saving habits and the value of money in her children from a young age

Keeping track of her children’s finances and allowance

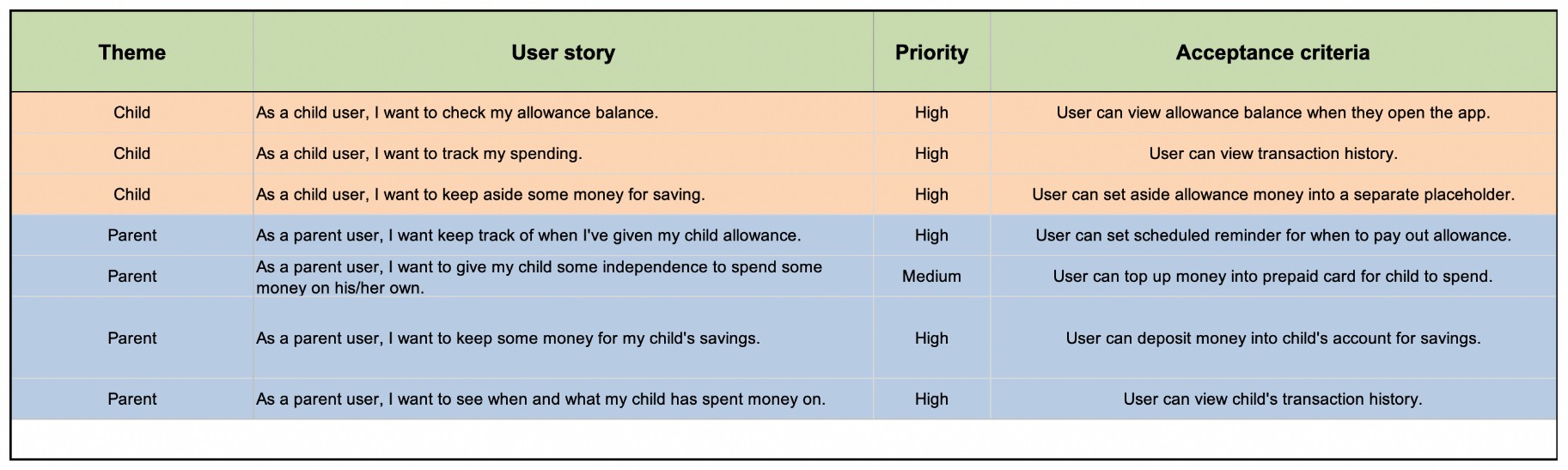

User Stories

Ideation & Concept

After studying the user personas and stories, analysing their pain points and goals, I came up with several ideations for features that would address their needs. I will be highlighting 3 major features for the purpose of this case study.

Serve as some sort of a virtual wallet placeholder.

Child can independently set aside some fund from Allowance into Coinbox as savings.

Keeps track of child’s spending as well as savings.

Parent user will be able to set scheduled reminder for allowance payout day.

Parents will have access to all 3 features and can deduct/add funds.

Parents will receive notifications whenever there is activity or transaction in app.

Serve as a virtual piggybank/coinbox placeholder for savings.

Child can track how much they’ve saved in their Coinbox.

Child can withdraw from Coinbox should they wish to use the money with Parents’ supervision.

Parent can also directly deposit money into Child’s Coinbox to boost their savings.

Training wheels for children in card spending! Children can learn financial responsibility by spending using cards without the burden of debts.

Only Parent may top up a preferred amount of credit into the linked prepaid card via online banking in app. Child’s Card account will then be updated instantly.

Parents can limit spending by depositing only a certain amount.

Children can have some degree of independence and control of their own spending.

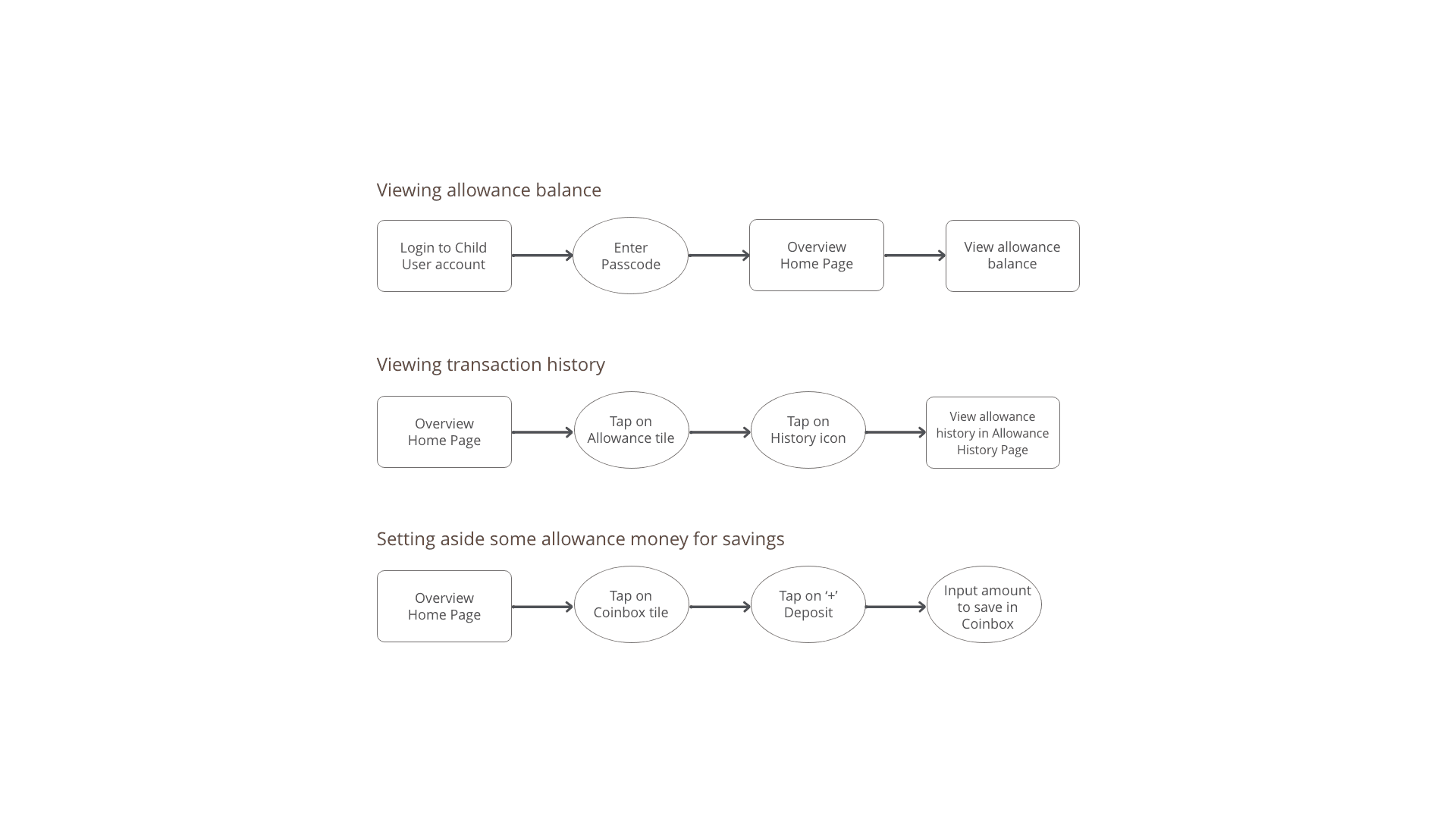

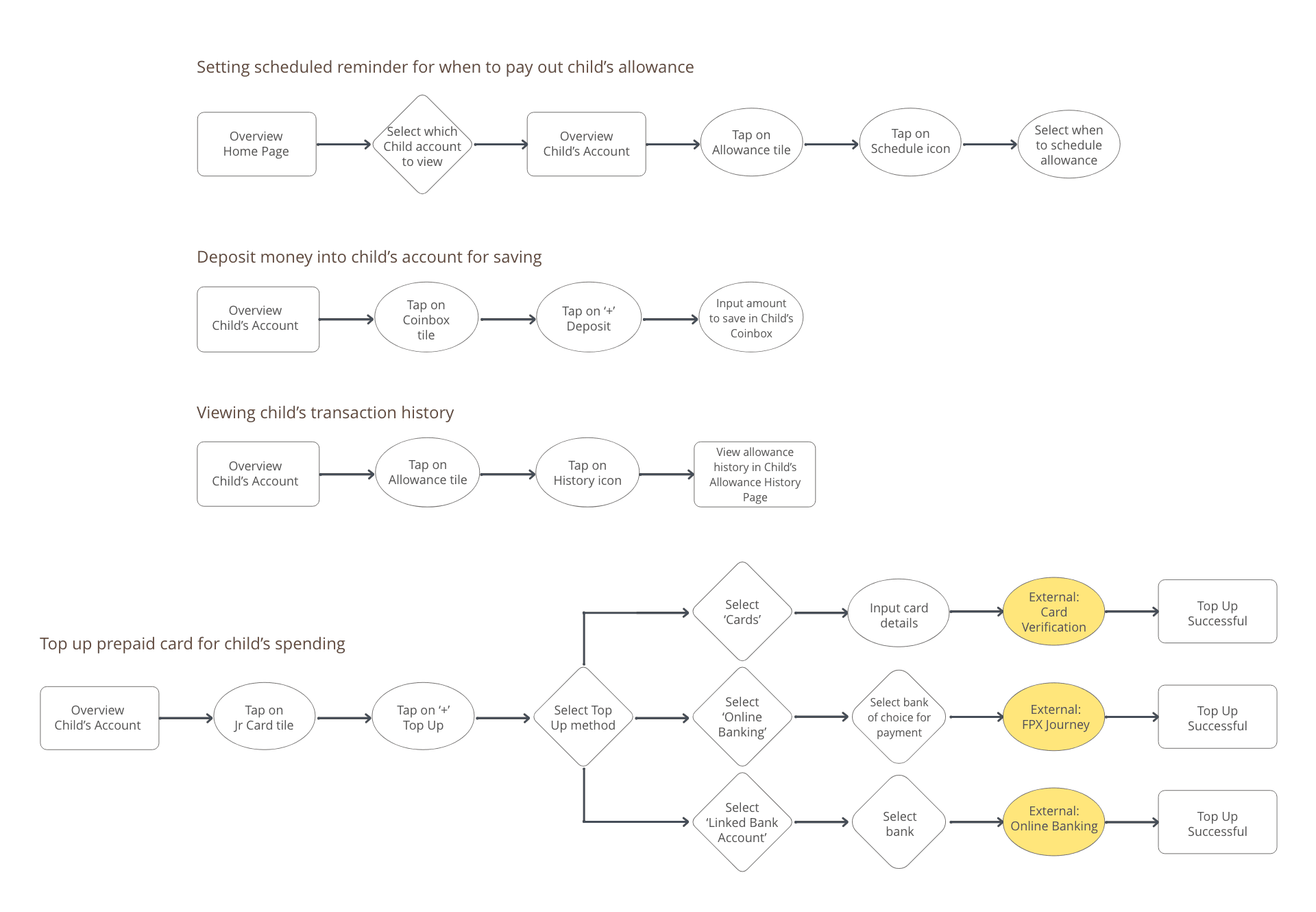

User Flow

Child User Flow

Parent User Flow

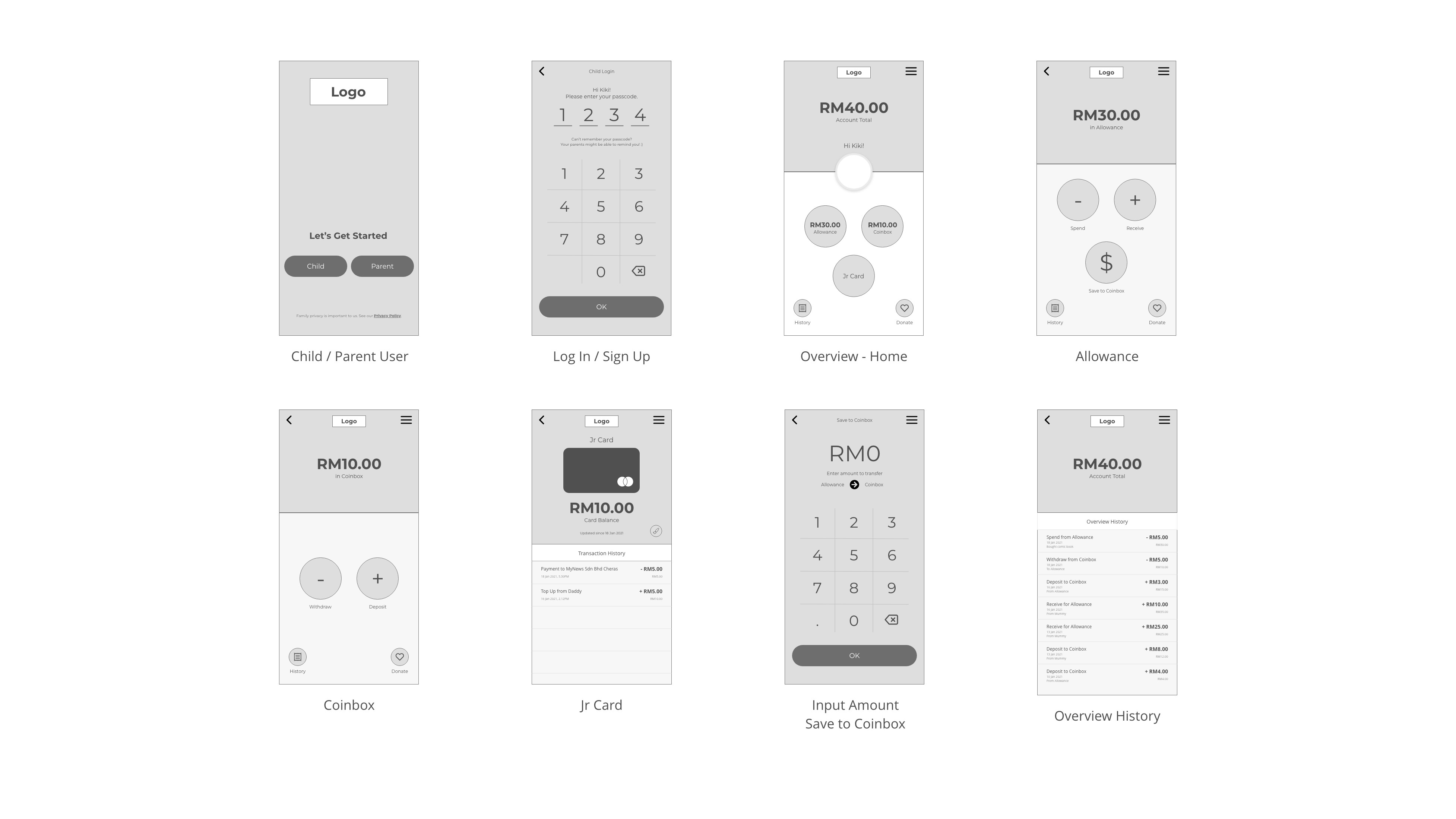

Wireframe

Child User Wireframe

Parent User Wireframe

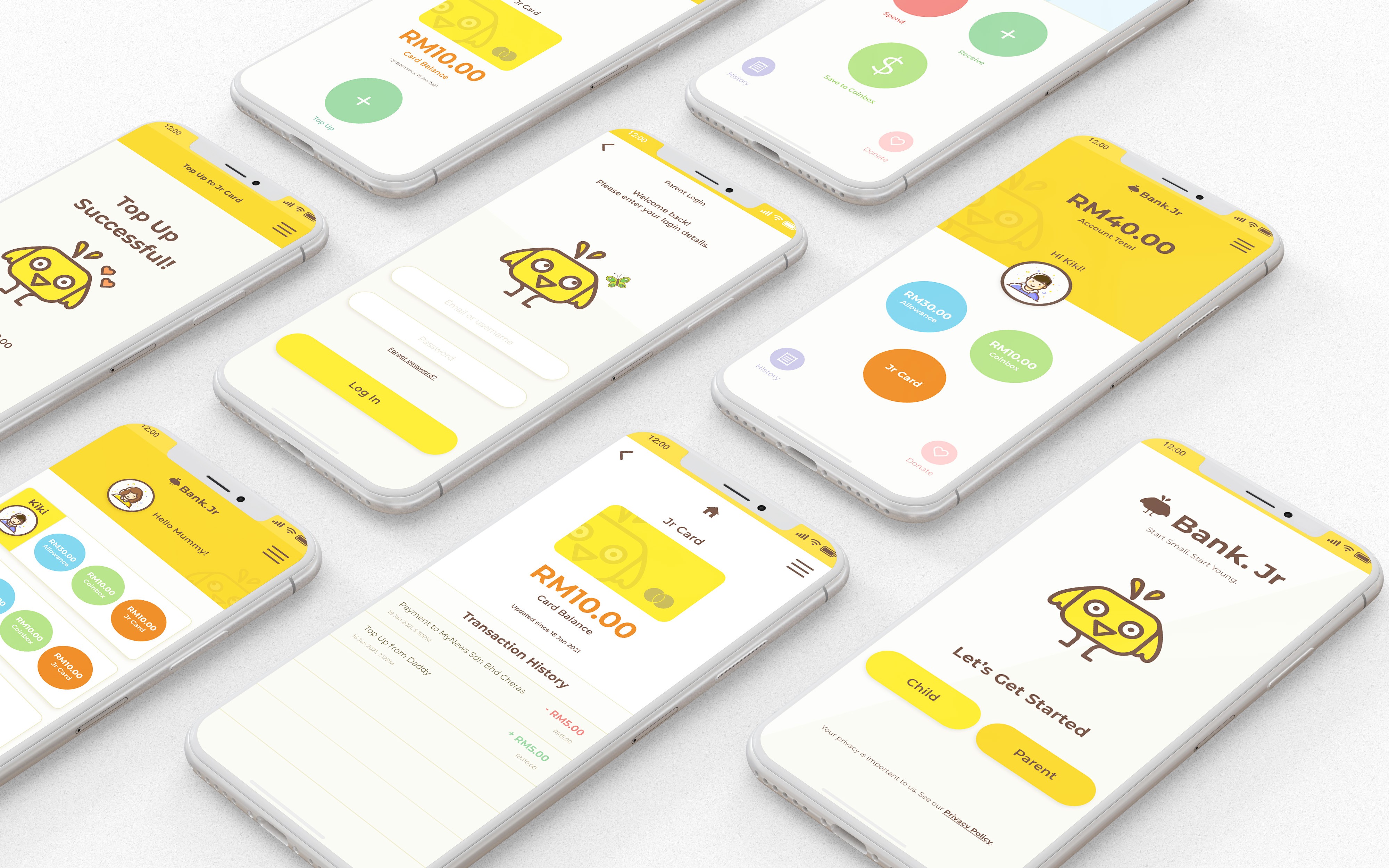

Hi-fidelity

Prototype

Appendix

“Habit Formation and Learning in Young Children” - May 2013, Dr. David Whitebread and Dr. Sue Bingham, University of Cambridge

https://mascdn.azureedge.net/cms/the-money-advice-service-habit-formation-and-learning-in-young-children-may2013.pdf

“Educating Your Children on Finances” - Legends Banks, US

https://www.legendsbank.com/news/financial-education-children/

“Tech-Savvy Toddlers: Why are Young Children So Good With Technology?” - February 2018, Southern Phone Co. Australia

https://www.southernphone.com.au/Blog/2018/Feb/tech-savvy-toddlers-kids-good-with-technology

“Exposure and Use of Mobile Media Devices by Young Children” - September 2015, Hilda K. Kabali, Matilde M. Irigoyen, Rosemary Nunez-Davis, Jennifer G. Budacki, Sweta H. Mohanty, Kristin P. Leister and Robert L. Bonner, Pediatrics.

https://pediatrics.aappublications.org/content/early/2015/10/28/peds.2015-2151

“Kids Will Be More Tech-Savvy Than Their Parents by the Time They Are 10 Years Old” - October 2020, VTech

https://www.prnewswire.com/news-releases/kids-will-be-more-tech-savvy-than-their-parents-by-the-time-they-are-10-years-old-301154064.html